Your Go-To-Market Works... Until Someone Audits It

Why growth breaks under scrutiny, and how to find your exposure before audit, IPO, or diligence schedules the conversation for you

The moment the music stops

There’s a particular silence that falls over a boardroom when audit asks a simple question and nobody can answer it cleanly.

Not a strategic question. Not a “where do you see the company in five years” question. A mechanical one. The kind that should have an obvious answer.

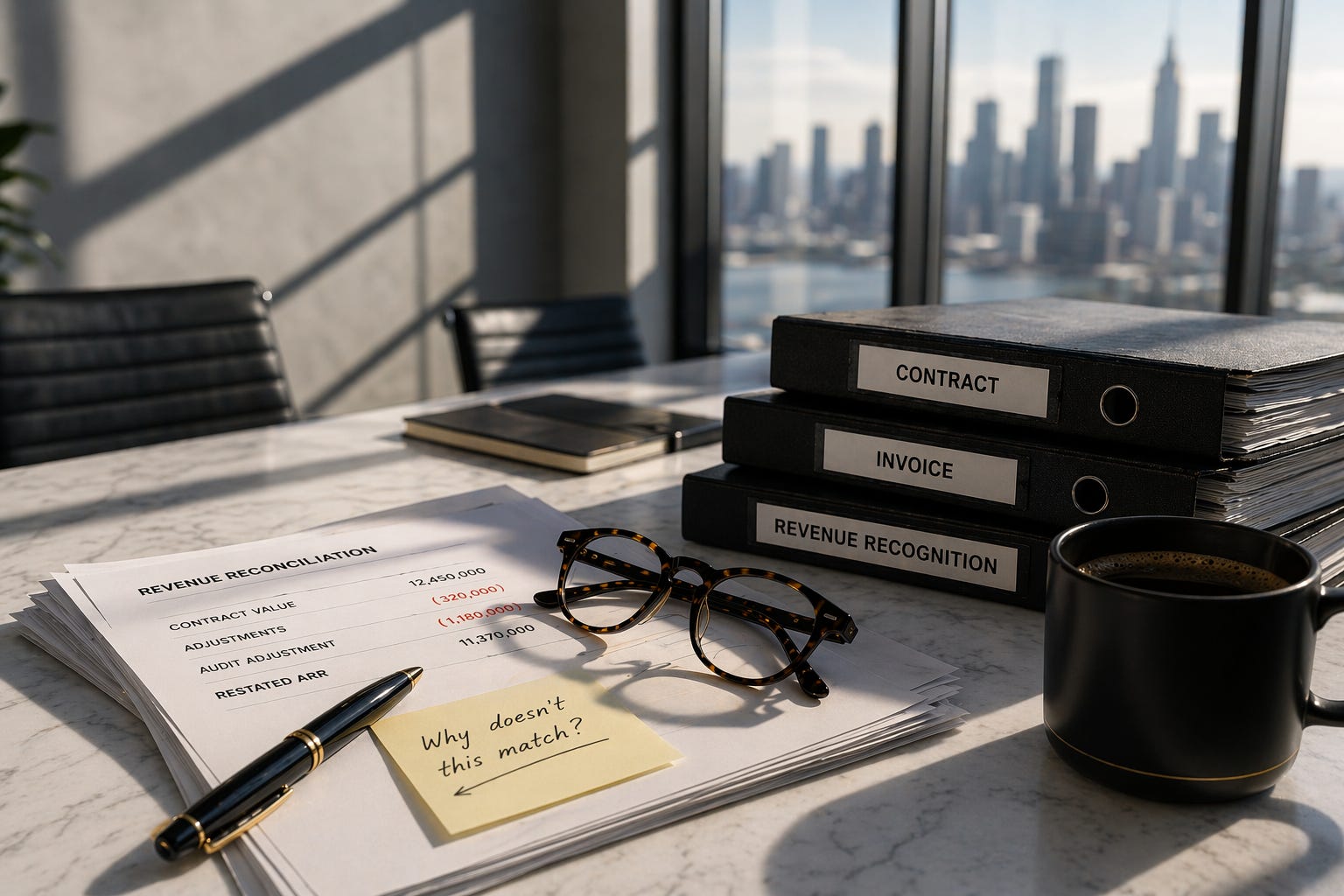

“Why does this contract not match the invoice?”

You’ve seen the face people make. The micro-pause. The glance at the CFO. The CFO’s glance at the CRO. The CRO who suddenly finds something very interesting on page 47 of the deck.

That silence isn’t confusion. It’s the sound of everyone in the room doing the same math simultaneously: how bad is this, and how many deals look like it?

Here’s the thing nobody tells you going in: audit didn’t create the problem. It just scheduled it. The conditions were set the day those deals closed, when the pressure was high, the quarter was ending, and the paper trail was an afterthought. Revenue looked clean because nobody was looking. Then someone looked.

That’s the whole story. And it plays out in board-level meetings across every high-growth company that scaled faster than its governance did.

The structural misalignment nobody names out loud

Let me make a counterintuitive argument: your sales team and your finance team are not misaligned because of poor communication. They’re misaligned because they’re supposed to be.

They were built to optimize for fundamentally different things. In different time horizons. With different definitions of success.

Think about the incentive architecture. Sales gets paid when the deal closes. The commission hits when the contract is signed, the CRM gets updated, and the champagne emoji goes in Slack. Nobody gets paid when the audit holds up six months later. The incentive clock doesn’t run that long.

Finance, on the other hand, is playing a different game entirely. Finance optimizes for defensibility, can this number survive inspection? Can it be traced, documented, explained, and verified by someone who wasn’t in the room? The CFO is not rewarded for narrative. The CFO is rewarded for things that are actually, verifiably true.

These are not the same optimization target. And in a high-growth environment, one side usually wins. Speed rewards the close. The board rewards ARR growth. The CRO gets celebrated. Nobody throws a party for documentation rigor.

So the paper trail gets thin. Deals get creative. Revenue gets recognized on optimism as much as obligation. Terms get added at the eleventh hour to save a deal that should have either closed on its merits or not closed at all. And the system hums along beautifully, right up until the moment it doesn’t.

This isn’t a character flaw in your sales team. It’s a rational response to an incentive structure that never asked them to think about what happens in quarter six. You built a machine that’s very good at generating bookings. You just haven’t checked whether what it’s generating can survive a question.

The three places GTM actually breaks

Here’s where the psychology gets interesting. When revenue integrity problems show up under scrutiny, they almost always cluster in one of three places. Not because companies are careless, because these are the exact spots where the pressure is highest and the accountability is lowest.

Deal construction: where drift starts quietly

Picture this. It’s 11pm on the last day of the quarter. Your AE has been working this deal for four months. The champion wants to sign. Procurement wants one more concession, nothing crazy, just a 60-day extended payment term and a small acceptance window on phase two. The AE has two options: push back and risk losing the deal, or say yes and figure out the paperwork later.

You know which option gets chosen. You’ve been in that position. The term gets added verbally. The contract gets signed. The CRM gets updated. The champagne emoji appears.

Three months later, someone asks what the customer actually agreed to. And the answer is: technically the contract, but also the verbal commitment, and there’s an email chain somewhere, and the AE has context on this...

That’s exposure. Not fraud. Not malice. Just a gap between what was agreed and what was documented, and the gap is now doing work inside your revenue figures.

Watch for contracts that don’t match invoices. Discounts embedded in deal structure rather than stated as line items. Terms added at close that weren’t in the original framework. The pattern isn’t dishonesty; it’s deal teams doing what they’re incentivized to do, which is close. The documentation is a problem for future-you.

Future-you is now dealing with audit.

Revenue recognition: where finance has to translate reality

IFRS 15 and ASC 606 are, at their core, surprisingly simple ideas dressed up in accounting language. The gist: you get to recognize revenue when you’ve earned it, when the obligation is clearly defined, delivery is confirmed, and there’s no credible reason the customer could reverse the transaction.

The pressure is always to move that moment earlier. Smooth the quarter. Reduce volatility. Book it now and sort out the details. And so you get revenue recognized on the basis of expected delivery rather than confirmed delivery. Deals where the milestones are technically unclear but everyone in the room knows what was meant. Multi-element contracts treated as a single block because decomposing them would move recognition out by three months and nobody wants to have that conversation.

Here’s the behavioral mechanism at play: the further you get from the deal date, the harder it becomes to challenge recognition timing. It would require someone to say, out loud, in a meeting, “I think we recognized this wrong six months ago.” That is a genuinely uncomfortable sentence to be the person who says. So it doesn’t get said. The number sits there. Revenue that needs a footnote to defend itself just quietly accumulates.

Until an auditor opens the folder.

The reporting layer: where stories diverge

This is the one that gets companies in the most trouble, because it looks so reasonable at every individual step.

CRM says the deal closed on March 28th. Finance recognized it in April because delivery wasn’t confirmed until then. Board materials reference the March close because that’s what’s in CRM. RevOps did a clean-up pass and reclassified the deal from Enterprise to Mid-Market based on contract value. Each of these decisions made sense to the person who made it.

Now try to reconstruct the deal from scratch. Which date is the real close? What was the recognition basis? What segment is it actually in? You’ll need four people from three different teams and at least one email thread from before Christmas.

That is the diligence nightmare. Not one big error. A constellation of small, individually-defensible adjustments that together create a system where no single number is fully reliable, and where explaining anything depends on who you ask.

Diligence teams don’t flag the individual data point. They document the pattern. And the pattern is what costs you points off your multiple.

What forces the reckoning

Most organizations don’t fix this proactively. Not because leadership is negligent, because the system actively rewards not looking. Deals are closing. The board is confident. The CRO is getting articles written about them in SaaS trade publications. Why would anyone want to be the person who raises the uncomfortable question?

There’s a psychological term for this: motivated reasoning. When the evidence is ambiguous, humans are remarkably good at interpreting it in whatever direction serves their interests. Revenue looks clean? We’ve got good processes. Revenue has some complexity? That’s just the nature of enterprise deals. The red flags don’t register as red flags because red flags would be inconvenient.

Four things break that equilibrium, all of them external, all of them forcing scrutiny you don’t control:

Audit failure. Adjustments cascade backward through prior quarters. The credibility gap with the board becomes a documented event. Your CFO is now having conversations they’d rather not be having.

Pre-IPO readiness. Revenue quality gets reviewed alongside revenue growth. Some of what looked like clean ARR turns out to require qualifications. The S-1 process is not where you want to discover this.

Board pressure. Once confidence drops, controls get imposed. Usually too late, and usually blunt instruments rather than precision tools.

PE diligence. This is the one with teeth. Deals get unpacked one by one. “Quality of earnings” adjustments are made. EBITDA gets normalized downward, sometimes materially. The gap between what management was projecting and what the numbers actually support becomes a negotiating position, which is a much less fun way to negotiate than starting from strength.

None of these created the problem. They just removed the ability to keep not knowing about it.

The 48-hour check (no transformation required)

Here’s the practical move. No new system. No consulting engagement. Just an uncomfortable afternoon with your Q1 deals.

Pull the last quarter’s material transactions, anything above your internal significance threshold. Take each one and answer three questions. The rule: you cannot use the word context in any of your answers.

1. Does the signed contract match what was invoiced? Not “mostly” or “in spirit.” Match.

2. Does the invoice match how revenue was recognized—and can you show the logic without calling the deal team? The phrase “the deal team would know” is not a pass.

3. Would finance describe this deal the same way sales would? If you’ve never actually tested this, the answer is probably more interesting than you expect.

What you’ll find breaks into three categories, and this is where it gets honest:

Clean — the deal is self-documenting. Someone who wasn’t in the room could reconstruct it from the paper. No call required, no context needed.

Explainable — the deal makes sense once someone explains it. Probably fine, but it’s high-maintenance under scrutiny and one key person leaving makes it fragile.

Fragile — the deal depends on interpretation, memory, or an email thread from nine months ago. This is your exposure. Not because anything dishonest happened. Because the gap between what occurred and what’s documented is now doing work inside your financials.

Most teams that run this exercise find more in the second and third categories than they expected. That’s not a scandal. That’s a signal. You now know where the soft tissue is before someone else presses on it.

The only standard that actually matters

The companies that make it through audit, IPO, and PE diligence intact aren’t the ones with the cleanest deals. They’re the ones with the most documentable deals, systems built so that any external party can reconstruct what happened without a briefing, an explanation, or the institutional memory of a deal team that may or may not still be employed there.

You don’t need perfect. You need self-explaining. There’s an important difference.

Perfect requires never making a complex deal. Self-explaining requires making sure that whatever you did is recorded clearly enough that someone outside the building can understand it six months later.

If you’re reading this thinking “we’d need to explain too many recent deals”, that’s not a red flag, but the answer. And the earlier you run this exercise, the cheaper the fix. Before the audit starts, you’re solving a documentation problem. After it starts, you’re negotiating with facts. Those are genuinely different situations with genuinely different outcomes.

The clock on choosing which situation you’re in is running. You just don’t know how much time is left.

P.S. The GTM Audit Pack (deal-level checklist, Red Flag Library with 14 documented failure patterns, Revenue Integrity Scorecard) is built for teams who want to run this exercise systematically rather than deal by deal. If three sections of this article sounded like your last quarter, the Pack tells you exactly how many deals they appear in, and what to do about it.

Get the GTM Audit Pack!

GTM Audit Pack: Revenue That Survives Scrutiny

The revenue problem usually appears too late to be called a surprise…